Web3 can be a confusing place. If you’re new, words like “blockchain,” “NFT,” and “smart contract” are opaque terms that do more to suppress curiosity than invite it. That skepticism shows up in the data: globally, just 1 in 10 working-age internet users own some form of cryptocurrency, the digital tokens needed to engage with much of the Web3 ecosystem.

This is ironic, since Web3 is the latest version of the internet, founded on ideas of accessibility and equity. Don’t let the critics fool you; the stereotype that crypto and NFTs belong to an exclusive and unwelcoming “crypto bro” niche is just that — a caricatured generalization. These tools are worth the learning curve no matter who you are (or how old you are) because they’re made with everyone in mind. And, just as crucially, they’re rapidly changing how the world works. While the blockchain — the technology underpinning all of what goes into Web3 — is indeed complex, the concepts it’s built on are actually pretty easy to understand. So, let’s dive in.

What is blockchain?

The blockchain is a distributed digital database that stores, moves, and tracks information globally without sacrificing transparency. This data is contained in “blocks” that link together to form a chain-like record of information flow. Think of the blockchain as a type of internet infrastructure. Just as the internet enables programs like Gmail, Spotify, or PayPal to exist, the blockchain allows apps and programs to run as well, albeit in a unique way.

Several blockchains exist, forming their own ecosystems online. Ethereum, Solana, Tezos, Flow, and Polygon are all separate blockchains. Blockchains are often referred to as a public ledger because their data transactions are available for anyone to see; no single institution or organization acts as a gatekeeper to the information they contain.

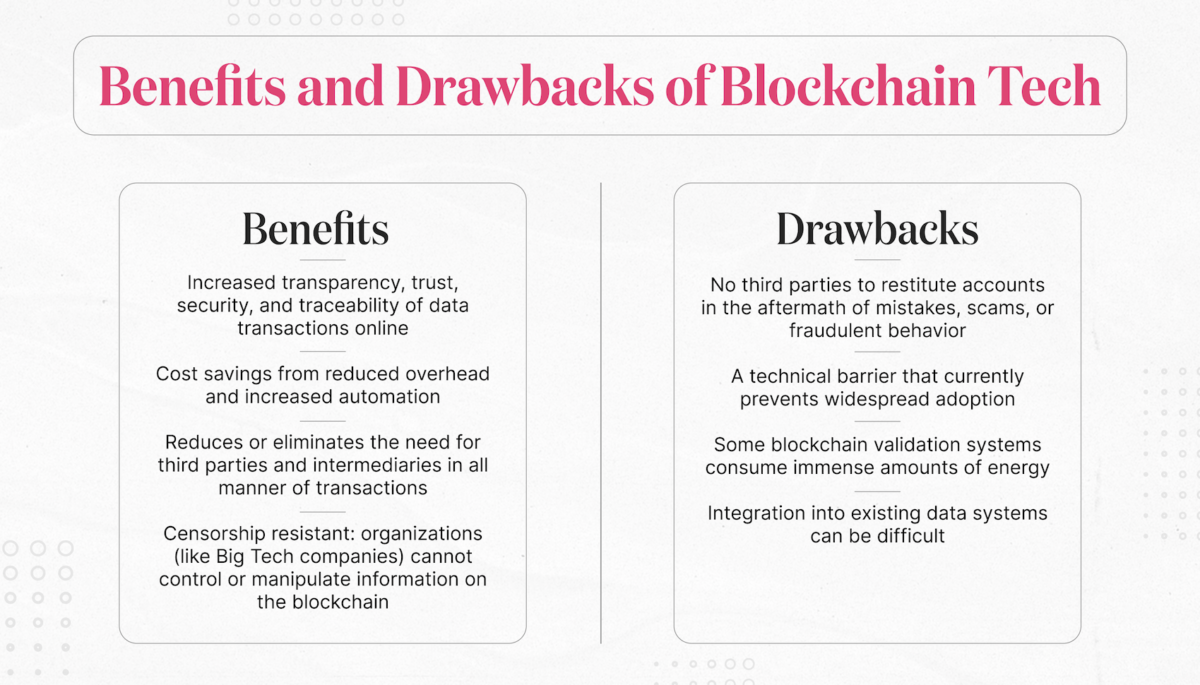

This is one reason why blockchain tech is so appealing to so many. Its openness and transparency contrast starkly with Web2 databases and systems operated by Big Tech entities like Apple, Google, and Microsoft, who control access to and can even manipulate their users’ data however they like behind closed doors. The decentralized nature of the blockchain produces an immutable and transparent record of data flow.

Alright, but what makes the blockchain so democratic?

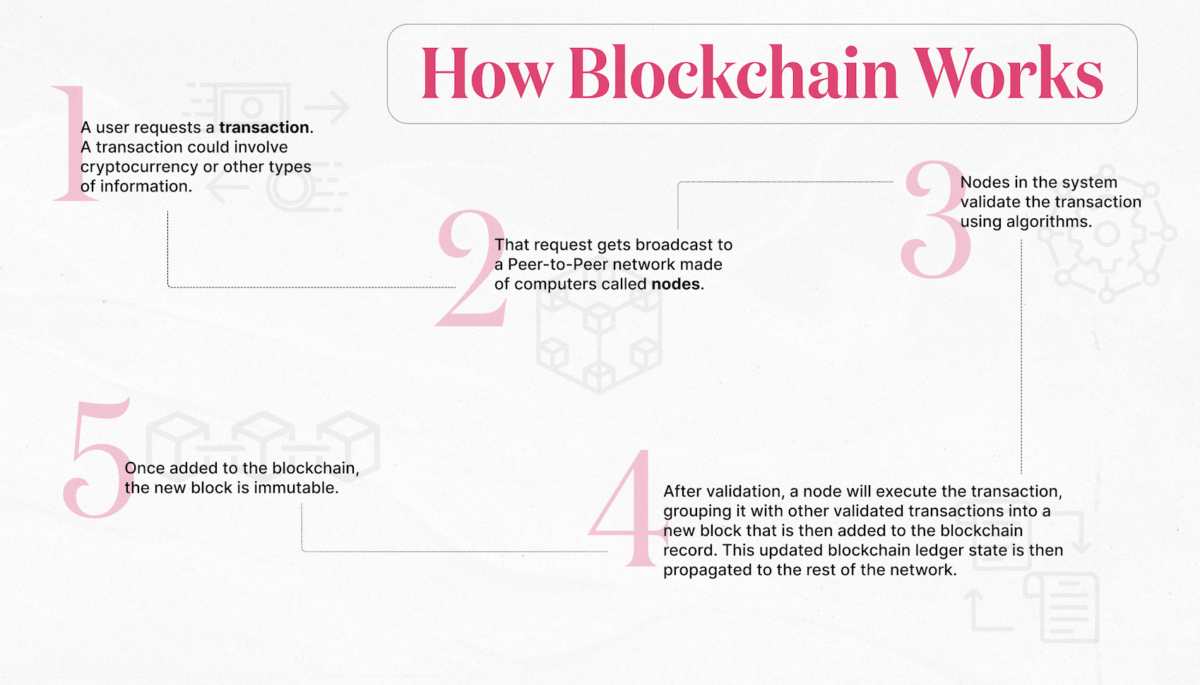

Blockchain systems are managed by a network of users. Rather than relying on a single centralized source, like Amazon’s data centers, for example, Web3 is operated by a distributed network of devices (known as nodes) running a particular blockchain’s software (like Ethereum) worldwide.

Data transaction records (like those of a cryptocurrency or NFT transaction) are stored in blocks that link together to form a chain of bookkeeping. Transaction requests are either validated or denied by majority consensus in the network. For a block and the transactions it contains to be officially and irrevocably added to the global ledger, the majority of computers (nodes) in the network have to agree on the transaction’s validity. This aspect of the blockchain is what makes it so secure and decentralized — no single individual or group can alter or obscure the information on it.

But what if someone hacks those nodes?

The core principle is that users in the system — not third parties like banks or tech companies — validate proposed transactions in that system. If I want to send X amount of cryptocurrency to a friend on the blockchain, users in the system who operate a validating node pick up on my request, validate its authenticity, and the transaction gets approved by the network as a collective.

Even if hackers gain control of a node to attempt a forged transaction (and steal someone’s valuable digital assets in the process), it won’t be recognized by other nodes in the system. In Ethereum’s case, hundreds of thousands of individuals and organizations running software around the globe act as that blockchain’s validators. To forge a transaction on the blockchain, hackers would need to take control of over half of those nodes — a near impossibility. Because of this, the more users running nodes in a system, the safer the blockchain is from being hacked.

Ok, so how does blockchain tech work, exactly?

So, now we know that blocks of data link together to form a chain of transparent and distributed record-keeping in this system. The next thing to know is that those blocks contain a few things.

The first is what’s called a cryptographic hash of the previous block. If that term freaks you out a little, you’re not alone, but don’t let it scare you. Cryptography is just the study of secure communication techniques that enable only a sender and receiver to understand its contents. And a hash is simply a way to compress data. A cryptographic hash, then, pairs the security functions of cryptography with the message-relaying abilities of a hash.

A block contains the cryptographic hash of the previous block to ensure that it hasn’t been tampered with. And a block will also include a timestamp, dating the transactions contained within it and the data of those transactions.

I’ve heard about smart contracts — what are those?

A Web3 staple, smart contracts are programs on the blockchain that run when certain conditions are met. Generally, these are used to automate the execution of an agreement without the need for a third party, as they are coded with instructions that only trigger in the right circumstances.

One well-known smart contract is Ethereum’s ERC-721, a data standard used for creating NFTs.

That all sounds great, but why use blockchain at all?

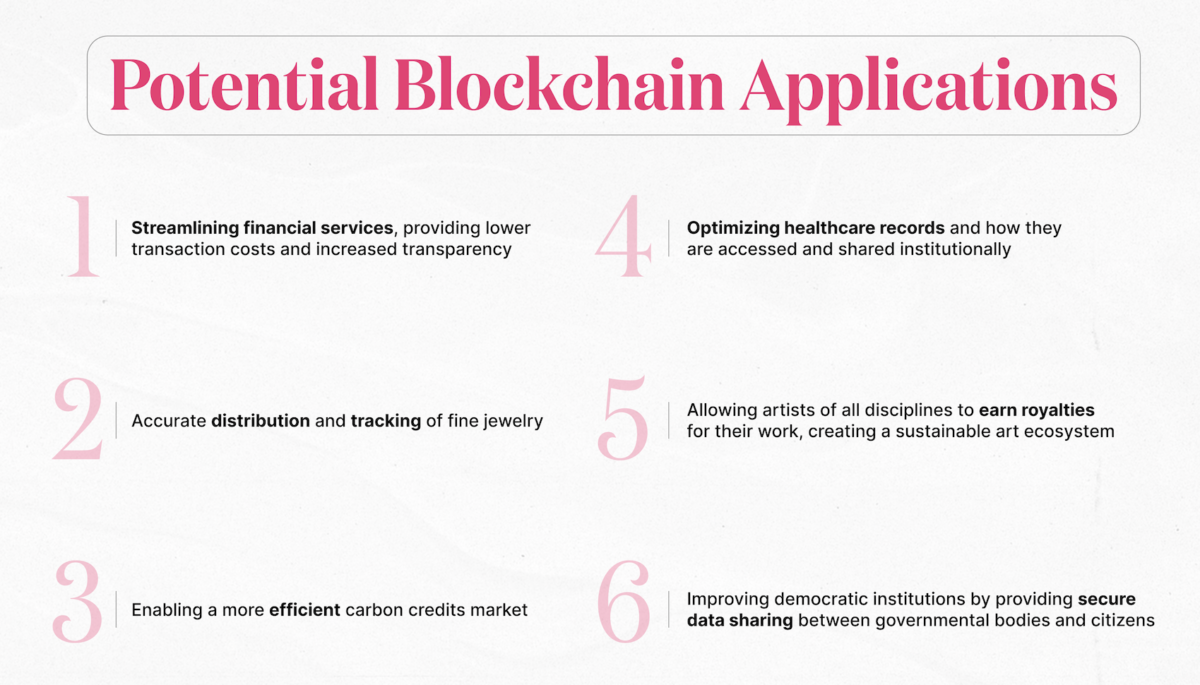

While blockchain tech is primarily used to enable transactions related to cryptocurrencies and NFTs, it’s only the underlying infrastructure for those functions. As such, that infrastructure can be applied in potentially limitless ways. The internet as we know it today enables applications and websites to function, but the internet itself is not limited to any one particular app or service. In the same way, organizations worldwide are exploring ways to utilize blockchain tech to improve and innovate in supply chain record keeping, data storage, payment processing, digital identification, carbon credit tracking, royalties distribution, healthcare, and plenty of other industries and applications.

Despite Web3’s difficult 2022, the technology that underpins the next version of the internet is simply too valuable and exciting to dismiss. As more institutions begin to experiment with blockchain tech, expect changes big and small to come to industries across the board. Web3 is still in its early days, and that’s all the more reason to learn about the technology before it gains widespread adoption.